Market Update and Auction Analysis – Early May 2026

A guide to the significant sales YTD, relative value changes and outlook

Summary

This year’s price action cannot be explained by the “end of an era” narrative

Ferrari has dominated the market in sales volume and largest price moves

There have been dramatic relative value changes

With momentum stalled, the market is at an inflection point

Overview

It has been a ferocious start of the year for the collectible car market, with some areas of extreme sentiment, volatility and dispersion. Despite geopolitical instability, values continue to be supported by macroeconomic conditions as the AI revolution remains the most important driver of economic growth and wealth creation (for example, ~75 OpenAI employees realising $30m in the latest equity round).

The “end of an era” narrative, suggesting that we are past peak car, has been pervasive, however, I am not convinced that it explains the price action we’ve seen. First, this is a generalisation driven by technical and regulatory developments affecting all manufacturers, yet the strength has clearly been concentrated and led by Ferrari. Second, it is not necessarily relevant to hypercars which are outperforming the market despite record primary supply. Last, while it is consistent with inverted generation curves, arguably this is at least as much a function of relative scarcity.

Rather, the 799 deliveries of the Ferrari F80 have begun and we have witnessed a reset of the relative value led by Ferrari’s new cars (see Ferrari market analysis). The sale of The Bachman Collection of extremely low mileage and distinctive Ferraris acted as a catalyst in January for the secondary market to catch up. Attempts to call other marques (e.g. McLaren) higher have not been lifted. It is testimony to Ferrari’s brand value that the price action has followed in this way.

There are emergent signs that the rally is stalling as sell-through rates have dropped. Examples of some of the unsold models from Monaco and Miami are going under the hammer over the next few weeks and will confirm whether it is healthy consolidation or a correction.

What has been trading, and which prices have moved most?

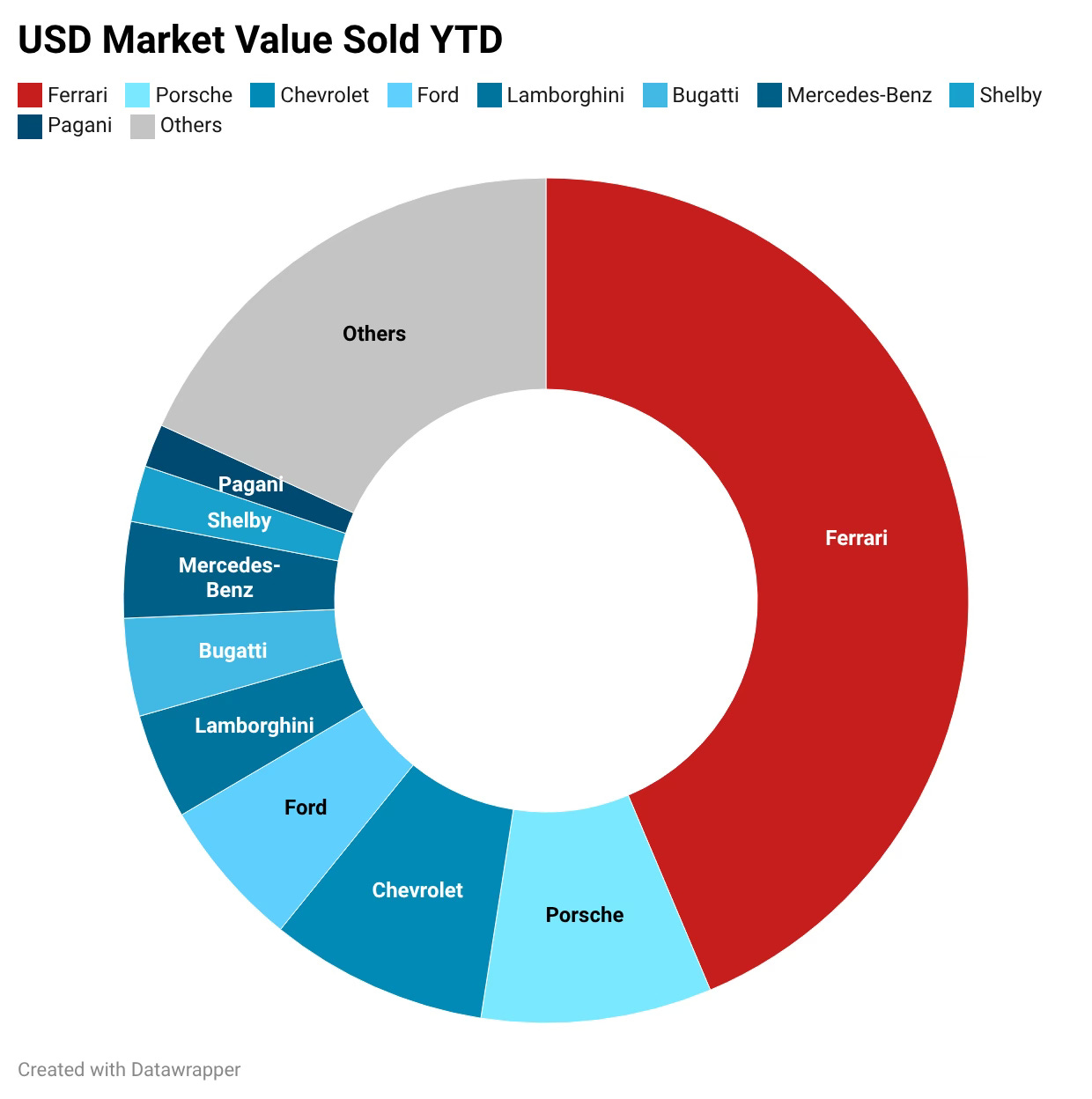

Perhaps unsurprisingly given the Bachman collection and subsequent price action, activity has been very concentrated on Ferrari: with >$550m in sales across major auction houses, the brand accounts for 44% of the USD market value sold YTD. 16 of the 20 most expensive cars sold have been Ferraris. The second most popular brand is Porsche with 9% of the market.

To consider which results have been the most surprising or market-moving, one can calculate Z scores. These measure the distance to mean as a multiple of standard deviations, therefore adjusting for market levels of variance due to factors like specification and condition. One would expect a unique low mileage car to trade with a Z score of at least 2.

The chart below shows the largest positive Z scores YTD, where I have sufficient historical data. Among others, the list contains many Bachman cars, an “Ispirazioni” special livery 812 GTS and a PTS Gulf Blue Carrera GT. However, these cars traded with more than specification or condition premia: the prevalence of Z scores greater than 10 demonstrates that this has been a structural repricing. The chart is topped by the Bachman British Racing Green 360 Challenge Stradale, a model line which has now ripped higher by a multiple of its previous value.

Wider context on this year’s rally

Considered over a long horizon, this year’s price action represents an abrupt change of gear, but it is not inexplicable. There are many macroeconomic reasons to suggest that the range-bound nature of the market between 2018 and 2024 was anomalous. Over this period, US M2 money supply rose +55%, the global market cap of crypto grew to ~$2.7tn and a revolution around generative AI began. Knight Frank estimate that the global number of UHNWIs ($30m+) almost tripled, from ~198,000 to ~713,000.

What the macro cannot explain is the degree of dispersion seen YTD, with the rally concentrated on Ferrari and other specific models which carry their own narratives and hype (for example, the Porsche Carrera GT). The chart below clearly demonstrates the dispersion seen between the LaFerrari and a small selection of other hypercars.

The significant auctions so far this year

Mecum, Kissimmee, January — the market gaps higher

The Bachman collection of very low mileage Ferraris sat at a rare intersection of two extremely popular market themes: unique specifications and modern classics. It acted as a powerful catalyst, forcing a repricing across these models.

Gooding Christie’s, Paris, January — Europe continues the rally

Not only did Europe confirm the jump in Ferrari values, but the positive momentum continued at Retromobile. Significant records set in Kissimmee were broken less than two weeks later: for example, the Ferrari 288 GTO record jumped from $8.525m to $10.911m (+28%).

Broad Arrow, Amelia Island, March — retrospectively, was this peak sentiment?

The breadth of the rally started declining with further gains very concentrated on specific models, leading to quite distorted relative value. For example, the Azzurro California F12tdf, which set a record at $4.185m, traded for 84% of the value of a similarly unused Monza SP2, and at a 10% premium to an F40.

Barrett-Jackson, Palm Beach, April — a more modern focus

As the top end of the market entered consolidation, interest rotated, allowing more modern cars to firm up. A record was set for the 488 Pista ($819.5k) while an SF90 XX, a current production car, cleared with an aggressive +70% premium.

Broad Arrow, California Mille, April – Gordon Murray T50

This single-car auction during the California Mille rally was notable because of the result achieved: the $8.035m price represented a +43% gain over a $5.63m print in December at RM Sotheby’s auction in Abu Dhabi.

Bonhams and RM Sotheby’s, Monaco, April — first signs of exhaustion

While stable, the market stopped setting new highs, with few surprising results across these auctions. Initial signs of exhaustion in Ferraris appeared with two 812 Competizione Apertas failing to sell, indicating discipline in the most modern cars.

Bonhams, Miami, May — consolidation or correction?

The most notable feature was the number of unsold lots; with momentum stalling in Monaco, opportunistic reserves were not met. Froth was clearly coming out of the market given the failure of the 335-mile Rosso TRS Ferrari F12tdf to sell, even at a reasonable discount to the Amelia Island record. Some interesting McLarens, for example the Lanzante P1 Spider, also failed to generate sufficient demand, demonstrating the brand concentration of the YTD moves.

Outlook

The market enters the summer period at an inflection point. The concentration of the YTD moves may not be sustainable, and short-term sentiment appears to be waning, yet the direction of travel is clearly supported by macroeconomics and financial market price action.

As production of hypercars remains very healthy, further gains are more likely to come from models which are not directly substitutable with this supply. Relative value across the market has changed substantially over only a few months and indicates areas of potential: the ratio of a LaFerrari to McLaren P1 is arguably stretched at more than 3x, for example.

There are several significant auctions through the rest of May, not least Broad Arrow’s sale at Concorso d’Eleganza Villa d’Este this weekend. The most interesting lots include the Pagani Zonda Unica (€9.5 - 12m) and Ferrari Daytona SP3 (€6.5 - 8.5m). The time series of especially topical cars including the Enzo, LaFerrari and 812 Competizione are about to be extended.