H1 Primary Market Report – No Scarcity of Scarce Cars

Analysis of the significant product launches and corporate events so far this year

Summary:

Manufacturers are responding to demand for the most driver-oriented variants and scarcity, two factors which have driven the secondary market YTD

The current primary market dynamics should have a dampening effect on recent secondary market price moves

Bullish: Aston Martin’s pivot to super sports cars, McLaren once uncertainty lifts

Bearish: Ferrari Special Series and Porsche GT3 on supply

This report considers each of the manufacturers with significant new product or corporate developments in the first half of this year. Positively, there remains a great focus on the types of models most in demand from enthusiasts and collectors, hence there is an abundance of rare cars. And, given that motorsport remains a lever to raise brand equity, it’s perhaps unsurprising that Aston Martin, Audi and McLaren are pushing this part of their business hardest.

However, the supply of series production sports cars is gradually being squeezed by fleet emissions targets, with the consensus profit-maximising strategy to concentrate on the EV and special ICE vehicle extremes of the business. This barbell strategy may maximise margins and is an attempt to perpetuate brand value in a tough competitive and regulatory environment. With primary supply focused on the most extreme parts of the market, it will naturally dampen the movements seen in the secondary market YTD.

Alpina

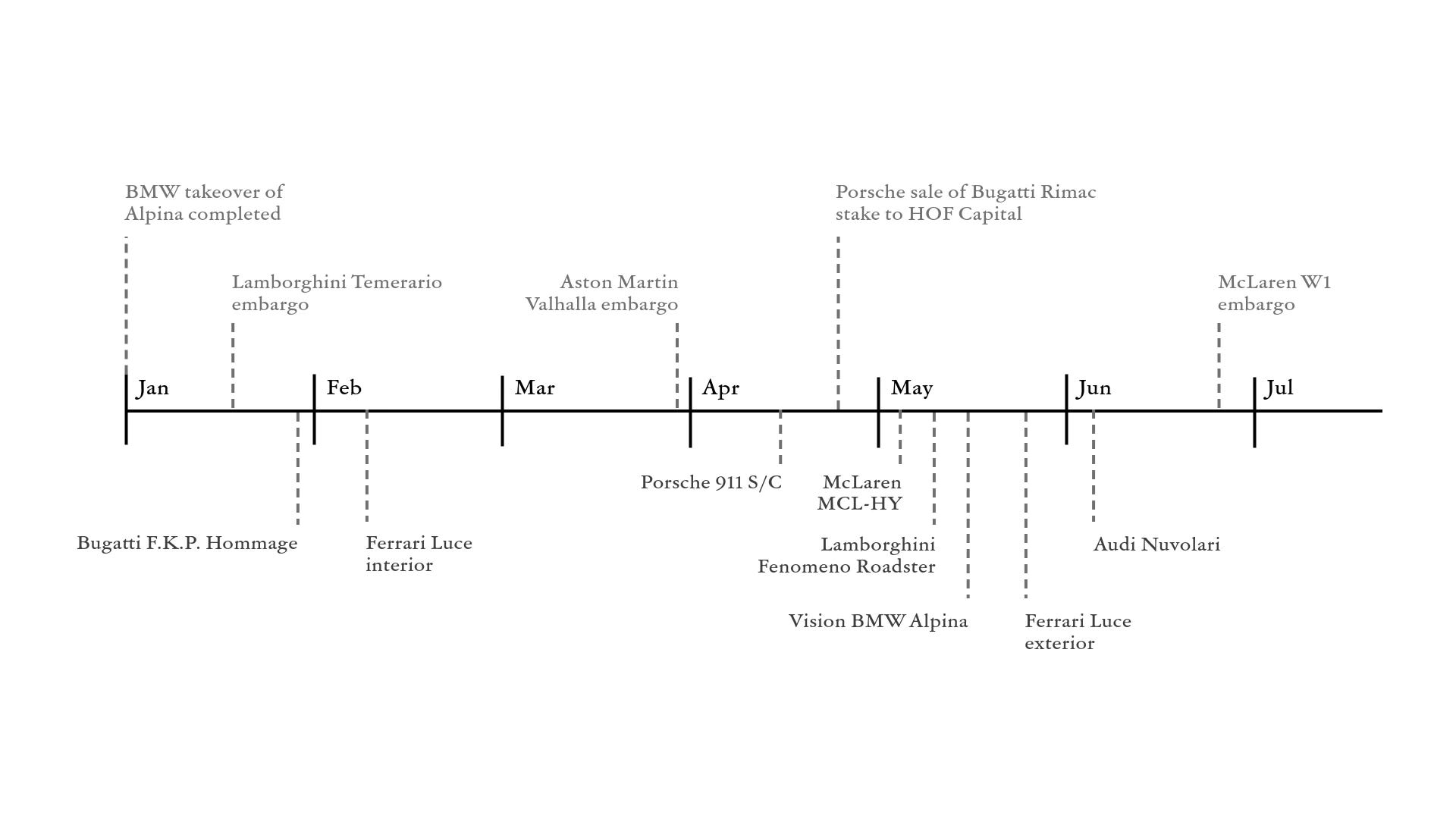

BMW revealed the Vision BMW Alpina at Villa d’Este in May, indicating their intention to take the brand upmarket to sit between BMW and Rolls-Royce. The first model will be “inspired” by the 7 Series. While in the same segment and price bracket as the Jaguar Type 01, BMW’s decision to fit the concept car with a twin-turbo V8 indicates that Alpinas will be powered by internal combustion engines for now. Clearly, the driver-oriented luxury saloon is a very small market segment, however, BMW’s track record reviving the Mini and Rolls-Royce brands bodes well.

Aston Martin

While Q1 deliveries were marginally down YoY and AML stock remains in a bear market (expensive capital structure), there are emergent positive signs. Most notably, the Valhalla media embargo lifted in March to extremely high praise, deliveries have begun, and the first public auction at Mecum’s Indy 2026 sale in May closed at $2.2m, a reasonable premium over list. While it has been a long gestation period and their initial experience with the Valkyrie was not without problems, the success of the Valhalla finally provides validation and confidence to pivot further towards high-margin, track-focused cars.

Aston Martin’s press releases are dominated by endurance racing, where the brand is having some success, unlike the separate Aston Martin F1 team. With increasingly aligned product and several competitor brands conspicuously absent from motorsport, it feels like an opportune time for Aston Martin to push its global brand recognition.

Audi

The Audi Nuvolari exemplifies how the market for sports cars has evolved over the past decade. Based on Lamborghini’s entry-level model, the Temerario, in some ways it is a third generation R8. However, unlike the R8, the Nuvolari will be limited to 499 cars and priced around €600k. Audi is clearly responding to the market: the high-volume territory previously occupied by the R8 has been monopolised by Porsche, while increasing value is placed on scarcity. Whether or not Audi can sell all 499 units, the Nuvolari is high margin and should lift the Audi brand ceiling which had been gradually falling since Dieselgate. Audi’s entry into Formula 1 puts it in a similar position to Aston Martin, pushing product value and motorsport ambitions to boost brand equity.

Bentley

Bentley’s tried and tested strategy of incremental updates continued with the launch of the Continental GT S and GTC S models in January, and a revised Flying Spur in June. Furthermore, the 500 new Supersports have been allocated. Rare Bentleys struggle to hold their value, even if they do perform significantly better than the series cars. The poor residual performance is a function of the incremental product strategy, as well as the luxury and GT segments they occupy. The commercial success of this strategy implies that any changes Adrian Hallmark brings to Aston Martin are unlikely to materially improve the secondary market value of their GT cars.

Bugatti

Porsche announced the sale of its stake in Bugatti Rimac to HOF Capital in April, marking an end to Bugatti’s VW era. HOF is a venture capital firm focused on tech; Rimac’s EV technology may have been their primary motivation. While clearly incentivised to maximise Bugatti’s brand value, outside VAG and under VC ownership there is likely to be significantly greater pressure to be operationally profitable on a standalone basis. For now, this may continue to manifest itself through Programme Solitaire one-off commissions like the F.K.P. Hommage. To the extent that the DNA of Bugatti’s cars changes going forward, the existing VW-era cars will be supported by their finite supply.

Ferrari

Ferrari has begun executing its barbell strategy with the launch of its EV, the Luce, which has dominated media following its exterior reveal. Ferrari’s intention to push the brand into new markets without cannibalising any of its existing business is evident from the product specification, as well as the design. The trend towards quiet luxury and the extent of wealth creation in the technology industry provide some justification for the strategy, whether it proves successful or not.

On the other hand, Ferrari’s upcoming product launches are aimed at its core enthusiast customer base and respond directly to the secondary market movements we have seen over the past year or two. Most notably among the cars widely rumoured, the 296 Challenge Stradale will be the lightest road-going variant of the model, without the hybrid system, while the 12Cilindri MM will offer an H-gated “shift-by-wire” manual gearbox, similar to the system used by Koenigsegg. These cars will be launched while Ferrari is producing the 296 Speciale in greater quantity than previous Special Series cars; this primary supply may signal a top in the part of the secondary market which has rallied hardest YTD.

Lamborghini

Lamborghini’s lineup of sports cars is very young, with the Temerario having joined the Revuelto this year. At Lamborghini Arena in May, the company unveiled the Fenomeno Roadster, limited to 15 cars following the 29 coupes announced last year. Around €5m, it is dramatically more expensive than any other special Lamborghini bar the Veneno, and more than 8x the price of a new Revuelto. There is a large gap between the primary and secondary valuation of few-off Lamborghinis which needs to converge if the brand is to be able to scale this part of its business. Without motorsport involvement, Lamborghini is leaning heavily on personalisation and individual scarcity to derive value.

McLaren

In May, McLaren revealed the MCL-HY, their 2027 endurance hypercar, and the MCL-HY GTR. This track-only car will be offered to VIP clients through the Project: Endurance programme, which includes access to the Le Mans racing team and six McLaren events. Last year in Abu Dhabi, Sotheby’s auctioned a bill of sale for $7.5m. Project: Endurance follows the success of Ferrari’s XX programme and complements McLaren’s return to racing in the top class of Le Mans.

Alongside the W1 supercar, McLaren is pushing its brand ceiling and average selling price during an otherwise quiet period for its series road car products. Last year’s merger with Forseven, a British EV startup, implies that they may be about to implement a barbell strategy similar to Ferrari. However, the layer of uncertainty at this inflection point for the brand is at least a short-term hindrance to valuations.

Porsche

Porsche pioneered the increasingly popular barbell strategy, which is embodied by this year’s specific product releases. Aside from the electric Cayenne, the most important launch was the 911 S/C, a cabriolet version of the 992.2 GT3. Importantly, unlike the S/T coupe and the 991 Speedster, it is not a limited production car. By building EVs, Porsche is able to push the highest margin variants of the 911, which have generally become significantly more accessible during the 992 generation. It is also a clear response to the secondary market, which places great value on naturally aspirated engines and manual gearboxes, although, as demonstrated by 992 GT3 residuals, relative abundance reduces the financial attractiveness of these specific cars.

It is also worth acknowledging the increased focus on Sonderwunsch, another strategy driven by market dynamics and designed to maximise margins. However, while their EV-GT barbell strategy may have led, the revival of Sonderwunsch follows the success of programmes such as Ferrari’s Tailor Made over the past decade.