Analysis of the market for Ferrari cars

Under the hood of the bull market and implications for the future

Contents:

Long term primary and secondary market performance and how this has been aided by Ferrari’s corporate strategy

Ferrari’s dominance of the hyper-car market, and its effect on older cars

The short squeeze in Special Series cars and updated relative value analysis

Market assessment of modern V12 Berlinettas

The price performance of the SF90 and implications for the 849 Testarossa

Ferrari has long been arguably the most successful sports car manufacturer in the world, however, perhaps less obviously, the relative performance of the marque has accelerated over the past decade. Ferrari’s corporate strategy has enabled its cars to outperform in a strong macroeconomic environment.

The market rarely moves in a straight line, and this year’s gappy price action demonstrates a lack of efficiency, even if Ferrari is probably the most liquid brand of the collectible car market. There is a lot of interesting relative value which will be explored later in this article.

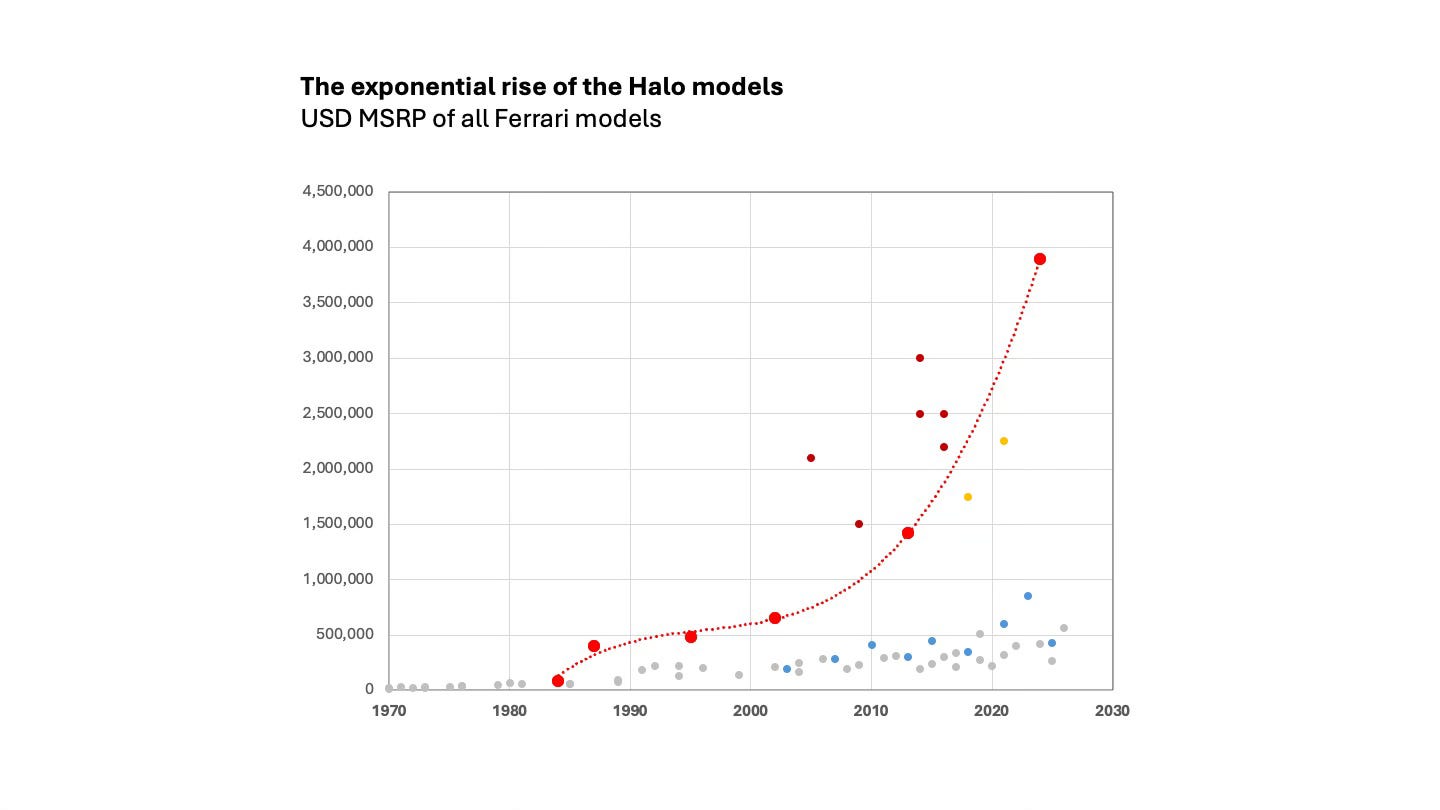

The long-term growth of Ferrari’s pricing power

Over many decades, through macroeconomic cycles and shocks, Ferrari has maintained its pricing power. Since the F40, the price of a new halo model has grown more than 6% annually; the CAGR has been closer to 9% since the Enzo. Importantly, this is genuine pricing power, as volume has grown concurrently, and the estimates are understated due to the cost of optional extras today.

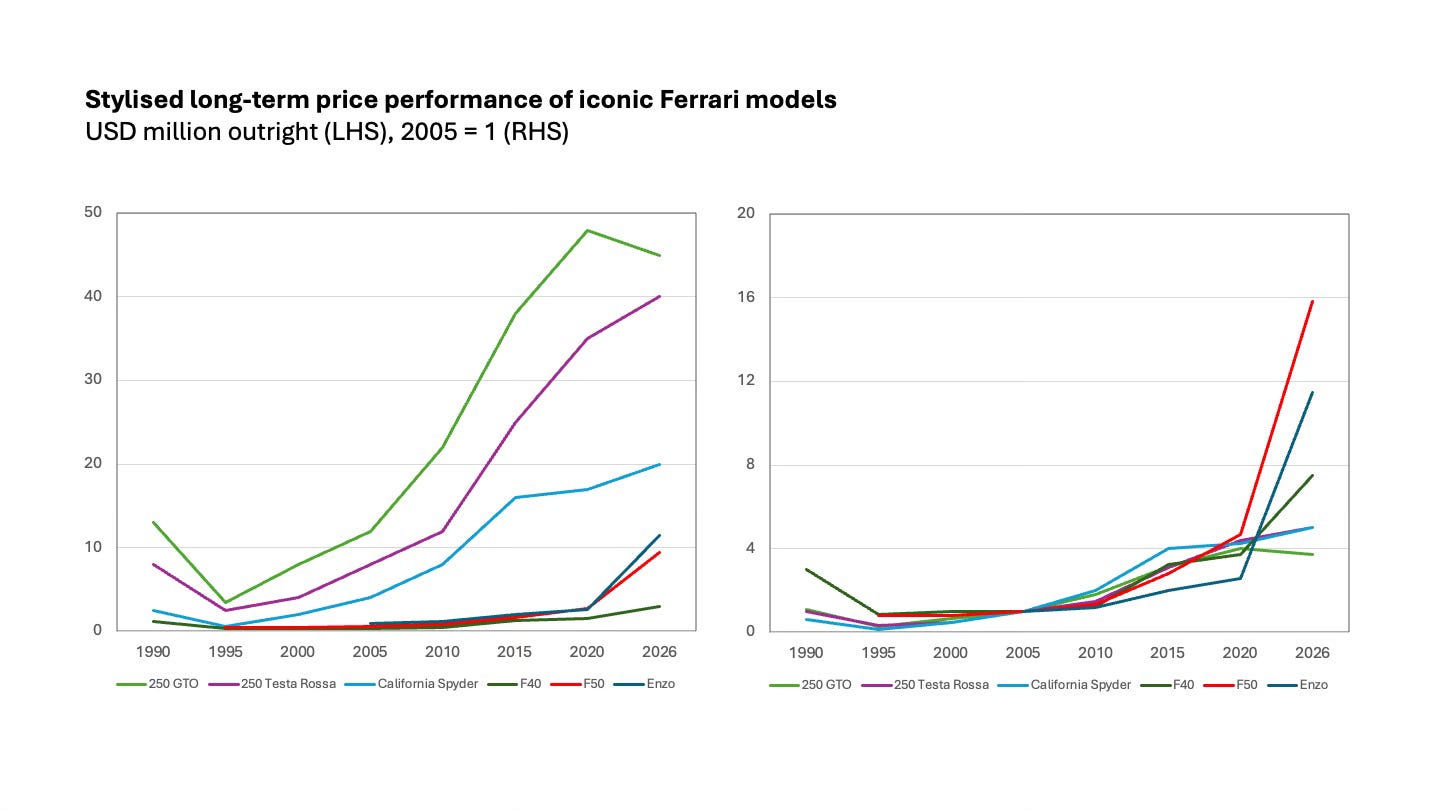

Long term secondary market performance

The strength of the secondary market for Ferraris really accelerated after the millennium, initially focussed on 1950s and ‘60s cars before broadening through the 2010s. The time it takes for any car to be considered a classic or collectible has diminished, and the best-performing parts of the market are no longer the absolute oldest cars.

Another way of framing this dynamic is that much of the long-term price performance has come from the gap between the primary and secondary markets collapsing. And generation curves have flattened, enabling the unloved belly – neither new nor classic – to dramatically out-perform over the past decade, benefitting the F50 in particular.

Ferrari’s strategy – supporting secondary values

The incentives of Ferrari SpA have generally been aligned with owners, and the company has managed a virtuous cycle where strength in secondary markets has justified aggressive primary pricing and vice versa.

It is not merely the characteristics and quality of the new cars produced that have maintained the brand. Ferrari remains very aware of its heritage, treating it as an asset which can keep compounding. There are several elements of the business which directly support this.

Firstly, the Classiche programme, launched in 2006, is important because it promotes the longevity of the outstanding cars; as the viability of long-term ownership improves, the terminal values of the assets increase. In general, long-term maintenance is an area where scale rather than scarcity improves the investment case (reducing the cost of carry).

The Corse Clienti department, which includes the XX programme and Ferrari Challenge, is another strategic complement that generates more value than its direct PnL. Facilitating customer track days and racing reinforces Ferrari’s motorsport links, helps sell cars, and is another example of the advantage of scale.

Lastly, the Icona cars elevate the brand and celebrate its back catalogue by saving retro homages for extremely special models, allowing series production cars to explore modern design ideas. That said, as controversy over the return of the Testarossa name demonstrates, Ferrari must be very careful in balancing forward- and backward-looking product ideas.

Outperformance in the hyper-car market

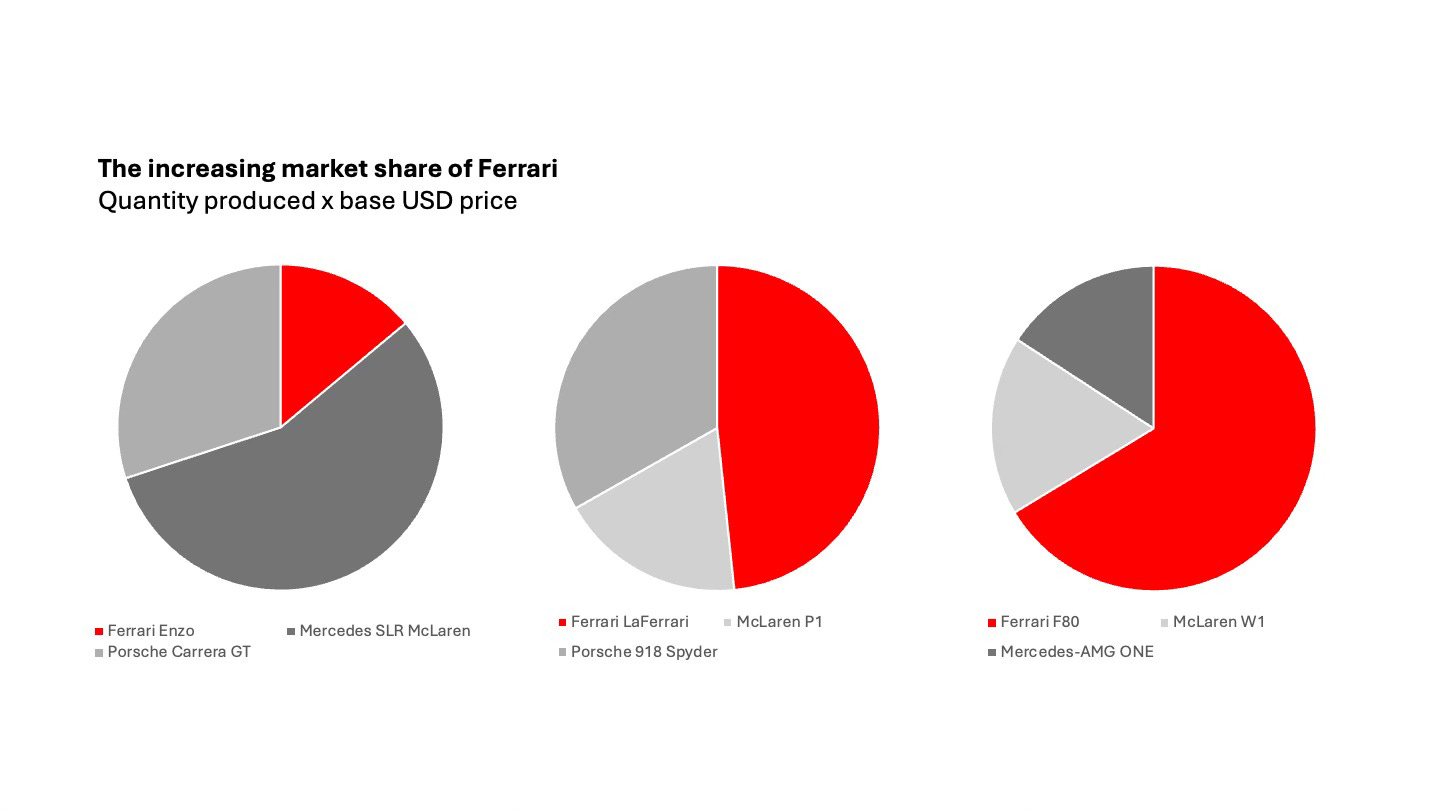

The hyper-car market is where Ferrari’s outperformance is especially stark: the company’s share of revenue has increased dramatically from the days of the Enzo to today.

The Ferrari Enzo production run was limited to 399 units, extended to 400 with the final car donated to Pope John Paul II. A relatively low production run set upfront is why revenue from the car represented a low share of the market but helps explain why its value has performed so strongly since. On the other hand, the Carrera GT and SLR both traded below list for quite some time. Porsche’s production plan of 1,500 units did not bind, as demand could only be found for 1,270 cars by 2006. Similarly, Mercedes-Benz and McLaren hoped to produce 3,500 units of the SLR in Woking over seven years, but demand could only be found for just over 2,000, including roadster and special editions.

The iconic “Holy Trinity” of the 2010s consists of three cars of similar ethos and business plan, and Ferrari’s share of the revenue was higher. With 918 units priced from around $845k, the Porsche was the most accessible of the three. An independent McLaren sold 375 P1s for at least $1.15m while Ferrari were able to sell 499 LaFerraris and 210 LaFerrari Apertas. More than $1.4m and $2m respectively, the LaFerraris demonstrated that Ferrari has the power to sell more units at higher prices than the other brands.

It is in the 2020s, however, that the success of Ferrari has become truly dominant. By selling 799 F80 coupes with a USD MSRP around $4m, Ferrari is collecting a very large share of the revenue available in this part of the market. It is testimony to the success of the brand that, unlike the cars a decade earlier, this group does not have a collective name and Porsche is absent. While the broader hyper-car market has expanded, other offerings remain very niche (for example, Koenigsegg produces only ~50 cars per year).

These charts help demonstrate the success of Ferrari to date, but it is hard to imagine the brand becoming an even larger proportion of this market going forward. To the extent that Ferrari has profit maximised, it is unlikely that the F80 generates alpha for its owners. And there is a clear opportunity for Porsche to return with a hybrid supercar and elevate its brand.

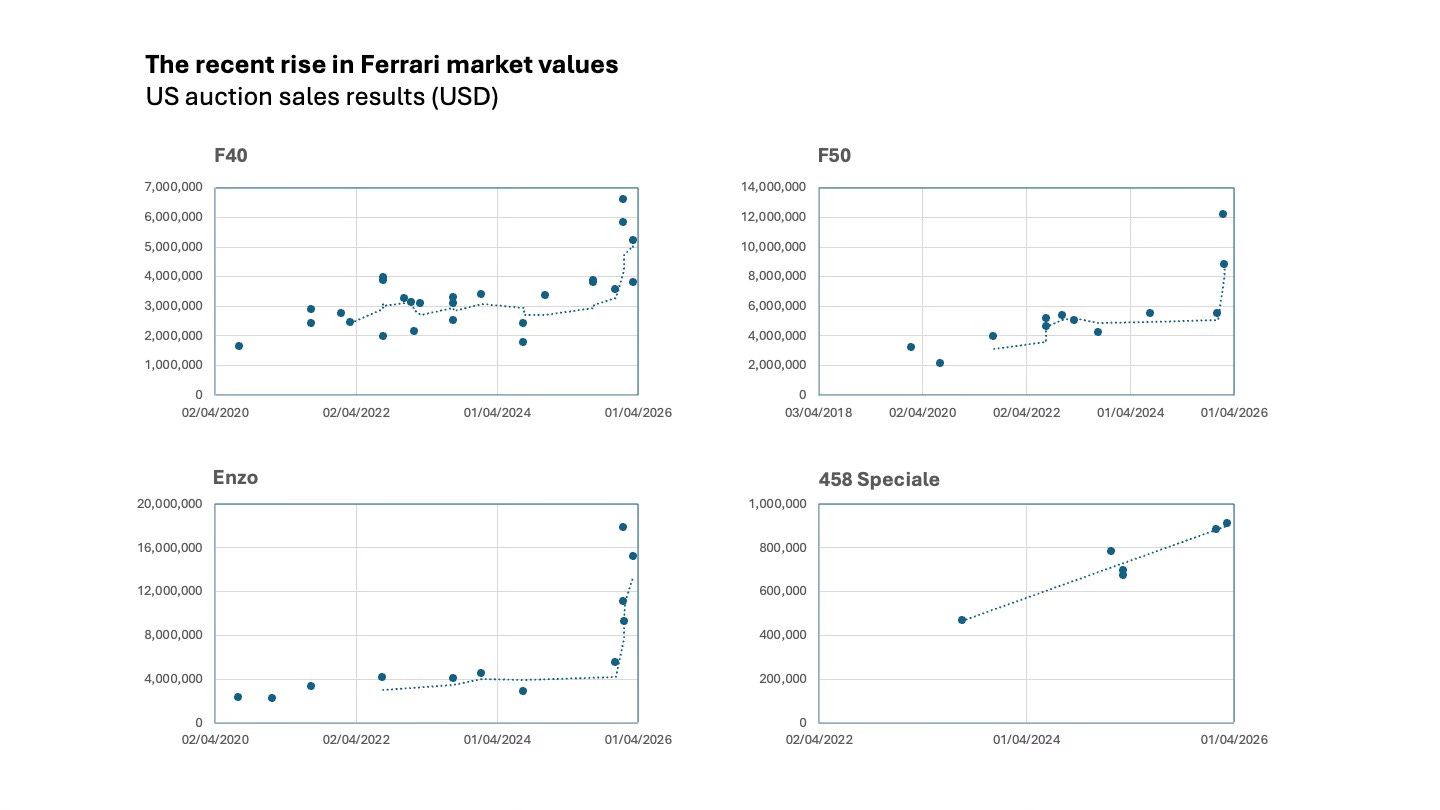

The recent rally

While the F80 is arguably fully priced, its production represents a significant clearing event which is now taking the rest of the Ferrari market higher.

Having remained stable through 2024 and 2025, the market for the most collectible Ferraris jumped in January 2026 with auctions held in Kissimmee, Florida. The Bachman collection was a group of extremely low mileage cars which had distinctive specifications from the factory, before personalisation was a common feature. The cars represented the very top end of the market, so the hammer prices were able to shock. The jump from previous auction results probably represented both the general values rising as well as the spread between the best and average cars widening.

A cautionary tale

While there are logical explanations and narratives justifying the strength of the market, today’s environment is exceptionally strong. The F40 demonstrates well the pre-GFC dynamics and could become a relevant comparison for the F80 in a negative state of the world.

Following initial euphoria, F40 values plummeted in the early 1990s and remained reasonably stable at the lows for a decade. Financial crises and recession did not help, however, the market nonetheless had to digest over 1,300 units – more than triple the initial 400 planned. The prevalence of cars meant that the F40 did not follow the macro recovery in the late 1990s experienced by other collectible Ferraris, and it remained significantly discounted to the F50 and Enzo which followed. This price path allowed many of the cars to be driven material mileage and indicates that it is not necessarily the historical norm for Ferrari’s supercars to be financial investments off the forecourt.

One should also consider the relative value inside Ferrari’s current range. The F80 is marketed at around 7x the price of a new 849 Testarossa. Although consistent with the outperformance of rare models in the secondary market, this is a very large premium compared to the historical pricing of Ferrari’s halo models: for example, the F40 launched at just over 4x the price of a 1984-91 Testarossa.

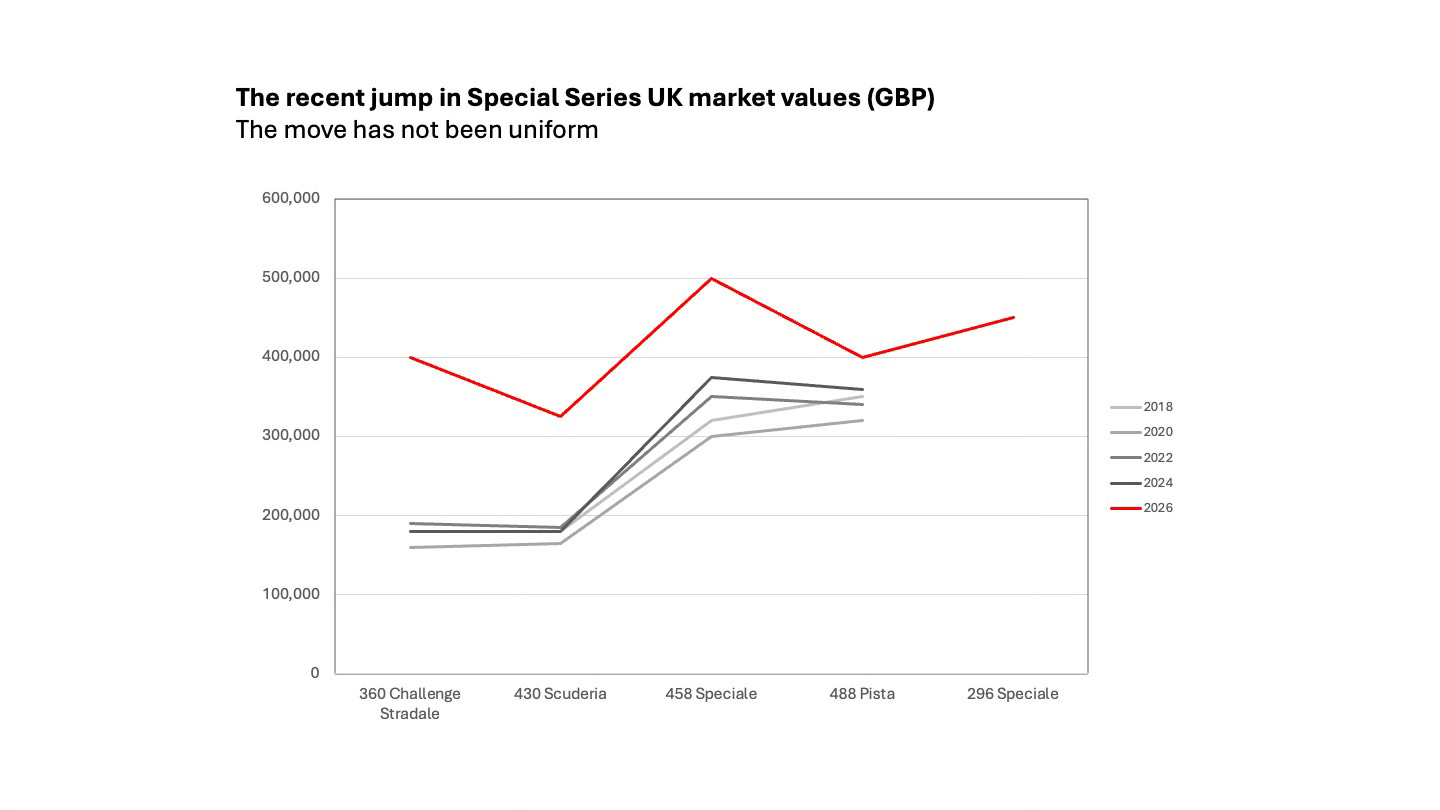

The Special Series short squeeze (UK market analysis)

Special series cars have been rallying globally. In the UK, this has manifested itself as a short squeeze over the past two months, with quoted values gapping higher from levels where the market had become bid-only. Clearing levels are likely to settle somewhere between the most opportunistic classified ads and prints earlier in the year. While the wider market is firm, there has been a very significant outperformance of these specific cars.

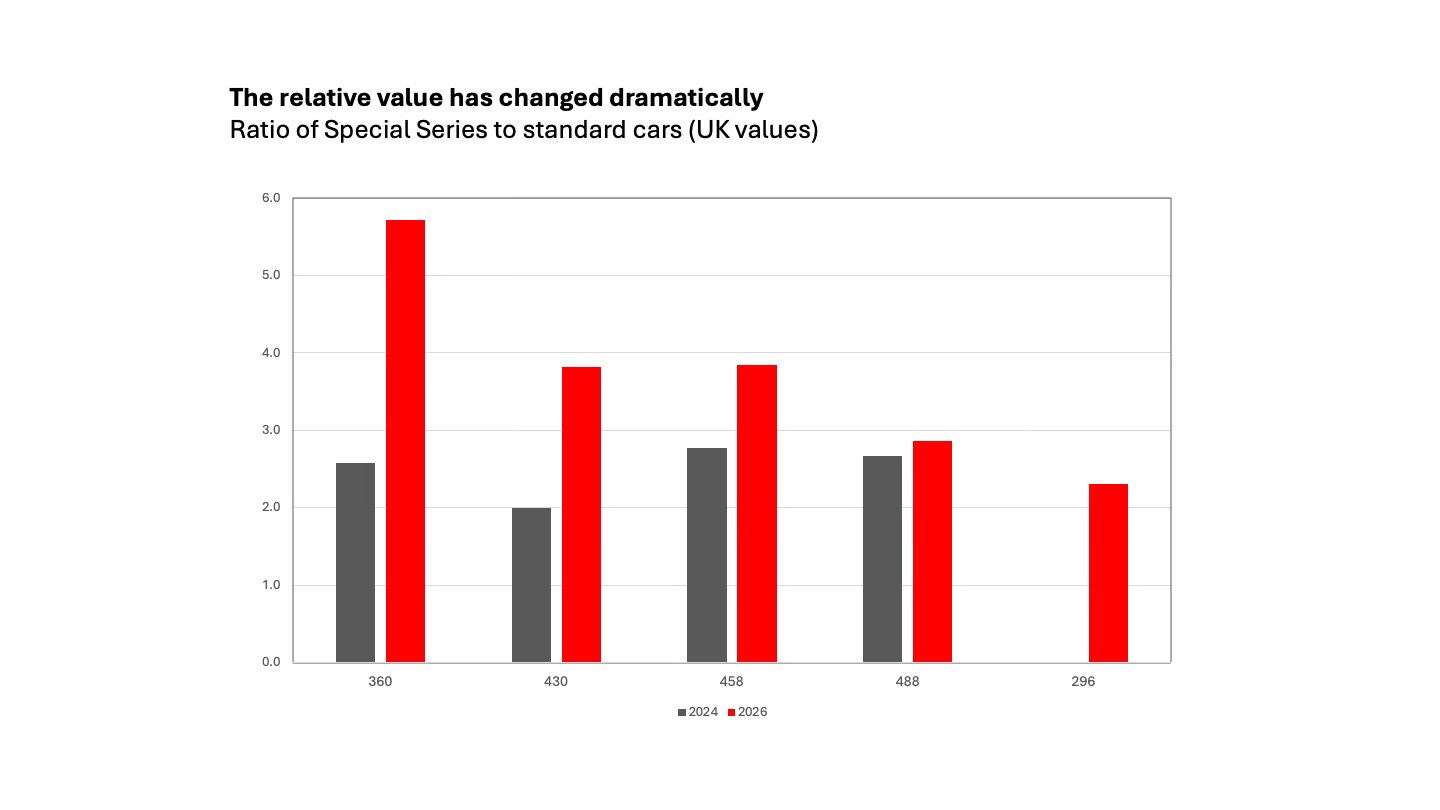

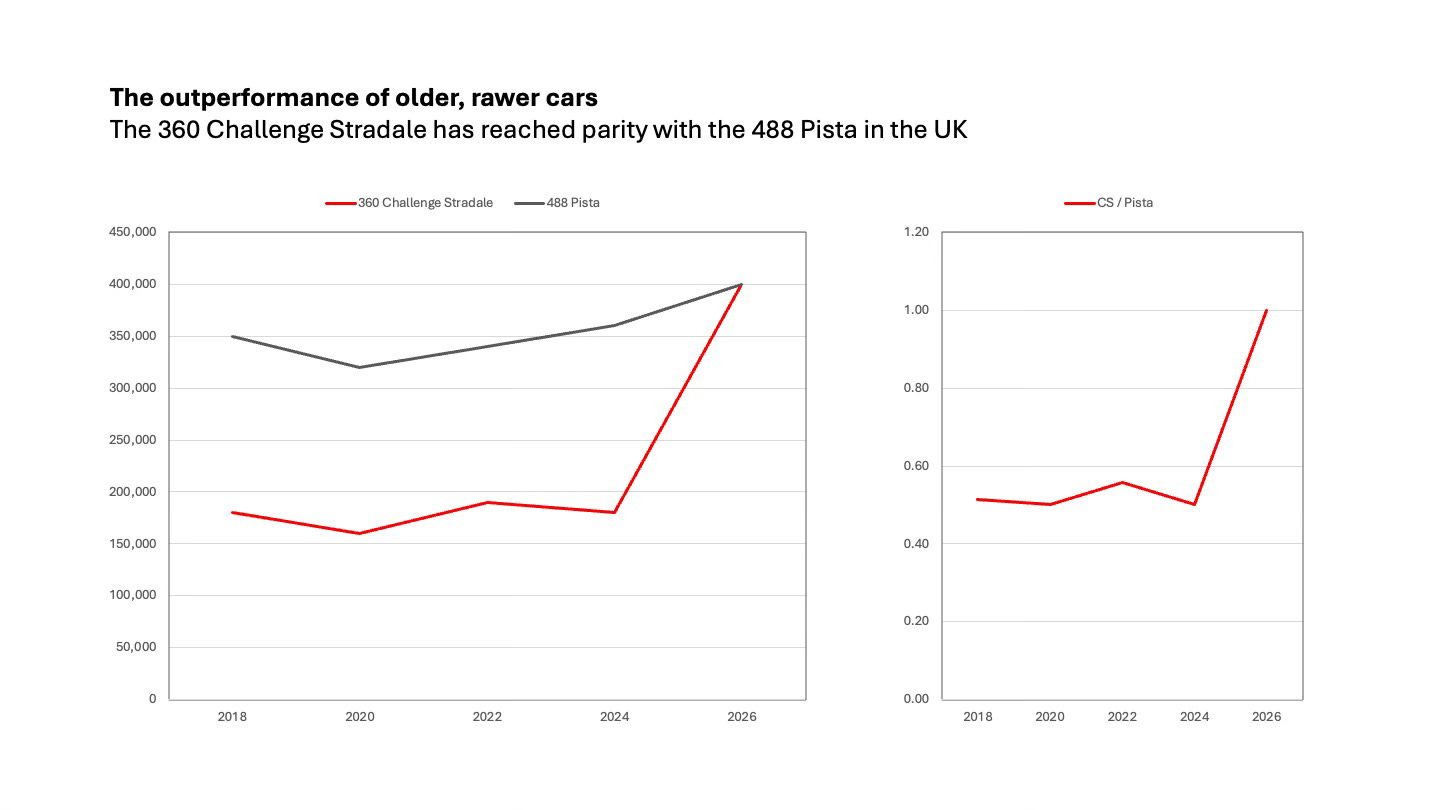

There has been a change of relative value within this group of cars too, some of which may be durable, and some will be faded. From a market technical perspective, with only 119 original UK RHD cars, the Challenge Stradale market can hold the new levels most easily, although liquidity will be extremely thin and the relative value is stretched. With prices more than +100% over the past year, the car has outperformed all other Ferraris. Over the past decade, most Special Series cars have traded between 2x and 3x the value of the standard cars; the CS/Modena ratio is now greater than 5x.

For comparison, 430 Scuderias and 458 Speciales are still worth less than 4x the value of the standard cars. Arguably the Scuderia is the best value of the Special Series cars here: reasonably rare (only 117 coupes and 41 16Ms registered in the UK) while offering a rawer driving experience than the later cars.

The 488 Pista market has under-performed the rest of the Special Series YTD (+11%). With 501 cars in the UK (29% of 488s here), it is inevitable that there will be a reasonable number of owners willing to switch into different cars as the relative value changes. The Pista market may gradually catch up but bear in mind that it is most closely substitutable with the new 296 Speciale.

The relative performance in the secondary market is giving Ferrari a clear signal to increase the supply of new Special Series cars, which generate higher margins, and the 296 Speciale is anecdotally more accessible than its predecessors. It is a very similar dynamic to the launch of the 488 Pista: the cars initially depreciated to settle at a discount to the 458 Speciale, however, once the period of indigestion was completed and the supply of new cars abated, the fundamentals became more important in determining long term value.

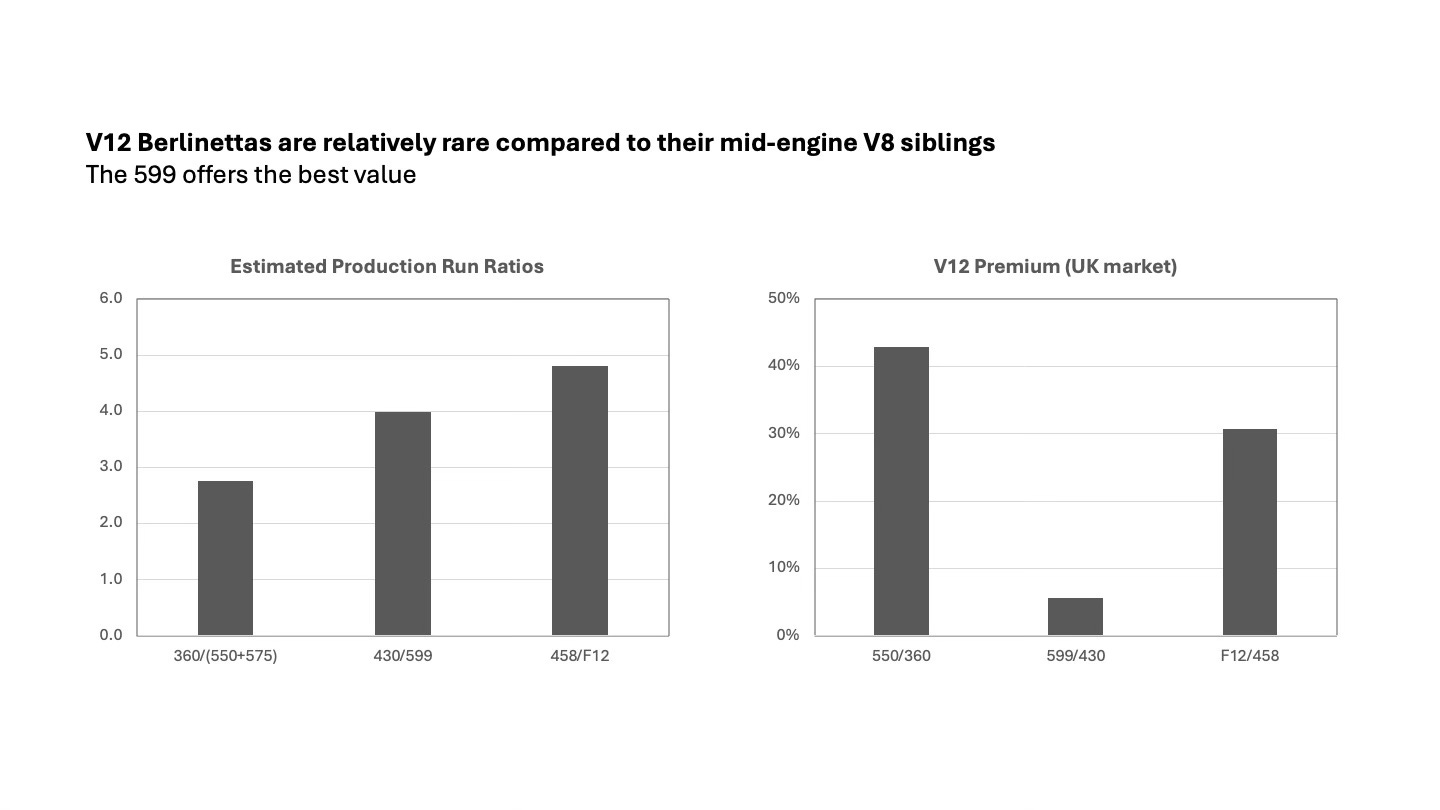

V12 Berlinettas are hiding in the background

There are many famous opinions and paraphrases of Enzo Ferrari. It is safe to say that he viewed the engine as the most important part of the car, had a strong preference for V12s, and believed that road cars should use a front-engine, rear-wheel-drive layout. The 250, 275 and 365 series of the 1950s-70s were powered by the Colombo V12, positioned at the front, and include many of the most iconic and valuable cars the brand has ever produced (250 GTO, 365 “Daytona” etc.). The front-engine V12 Berlinetta is therefore as close as anything to the epitome of Ferrari.

Front-engine cars are currently discounted in the collectible car market, which places a premium on the mid-engine layout, perceived to be more dynamic and favoured for track driving. It is worth bearing in mind that this market pricing is not permanent.

The Ferrari 550 Maranello was unveiled in July 1996, offered from £143,000 in the UK and slightly over $200,000 in the US. In the UK, a 550 was worth 10-20% more than a F40 at the time! Ferrari built 3,083 coupes and 448 Barchettas, so there are just over two cars for each F40 in existence. The 599 is also a relatively rare car but, for comparison, there are ten for every Enzo in existence. With 457 Ferrari 550s delivered new to the UK, the car is rarer than a 488 Pista. Indeed, Ferrari’s V12 GTs arguably trade with little premia considering how much scarcer they are than contemporary mid-engine series production cars.

Given relative scarcity, heritage, and reasonable market values, I believe that there is scope for modern V12 Berlinettas to appreciate – especially the 599 which trades with less than 10% premium over the F430, despite being 4x rarer.

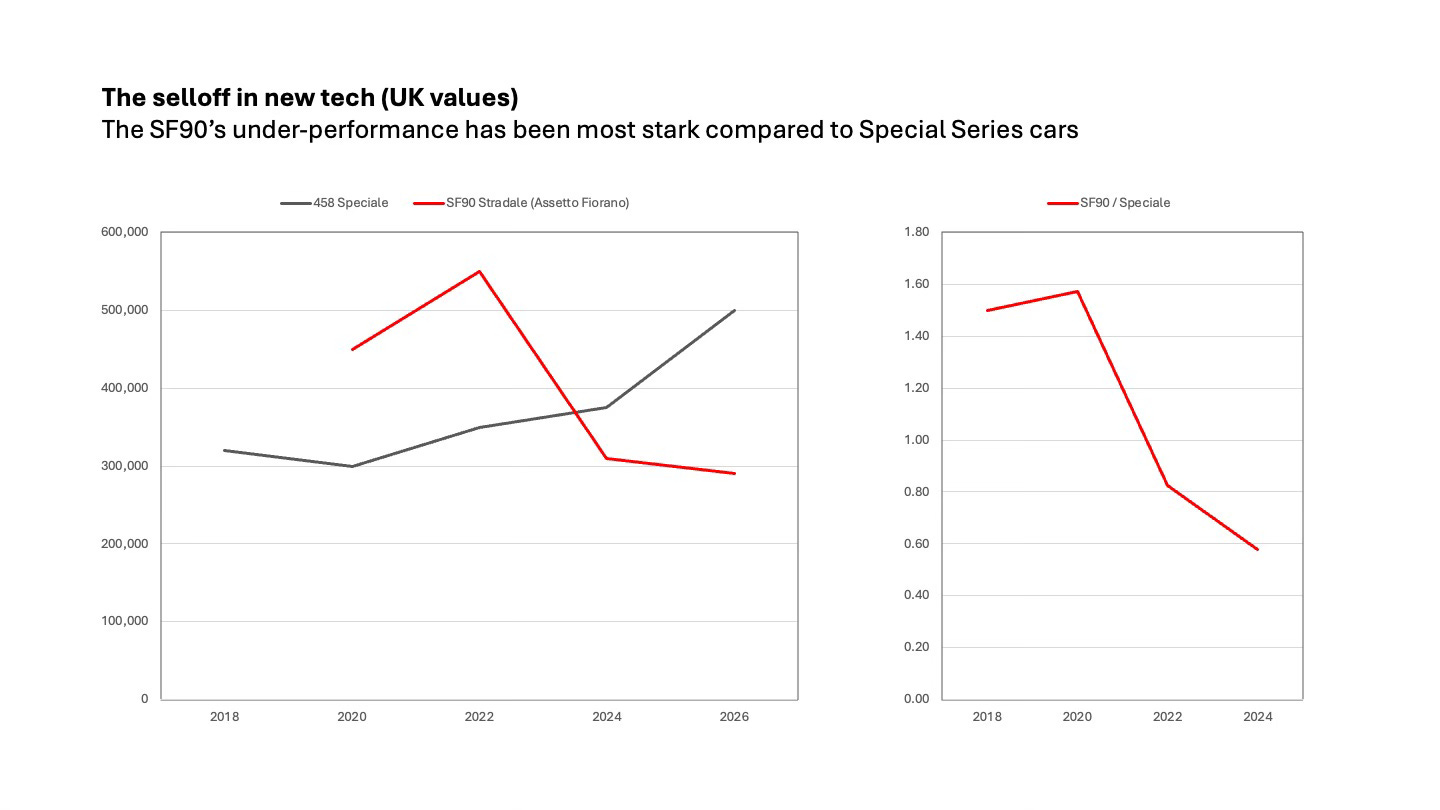

Is the SF90 a sensible long yet?

The under-performance of the SF90 has been dramatic, even compared to the 296. The selloff represents a combination of usual series production car indigestion, negative market sentiment relating to the hybrid system, and a correction from the euphoric post-COVID environment.

To ascertain whether the SF90 offers some value here, we can compare it to a potential floor and ceiling: currently, it trades 30% of the distance between a 296 and a new 849 Testarossa. This feels like a reasonable valuation, however, both goal posts remain depreciating assets. I expect the SF90 to ultimately settle at least equidistant, primarily driven by depreciation of the Testarossa.

Although power output remains an important driver of new car prices, the secondary market is becoming less sensitive to this parameter. Thus, models like the 849 Testarossa, the replacement of the SF90, sit in an uncomfortable position: the secondary market may not support its premium placement in the current range. This does, however, imply that the model may end up relatively scarce for this era of series production Ferrari.

It is worth noting how relative demand for hybrid models is influenced by government policy. To the extent that taxes and restrictions are focussed on the sale of new cars – for example, France’s Malus Écologique (ecological penalty) of up to €80k, or the UK’s planned ban of pure ICE cars from 2030 – the secondary market for hybrids will continue to under-perform. It must digest more primary supply while pure combustion cars become rarer. Therefore, while unlikely, a bullish scenario for hybrid values exists if the balance of policy shifts away from restricting the primary sale of pure ICE cars and towards taxing their use.

A few more observations:

A lineup of highly distinctive cars with short product cycles appears to be a good strategy for maximising both shareholder and consumer value

The recent steering wheel retrofit, replacing haptic controls with physical buttons, demonstrates a very positive approach to customer feedback and long-term support of car owners

Ferrari’s pragmatic EV strategy is evidence that the company is very alert to the risk of diluting its brand

The partnership with LoveFrom, signals a willingness to explore new ideas, a sign of both strength and the inherent challenge of developing an emotive EV sports car

The most successful period for Ferrari’s road car business has coincided with an almost 20-year F1 championship dry spell

That said, Ferrari’s recent success at Le Mans has no doubt helped give credibility to the V6 hybrid powertrain in the F80

Perhaps allocation-driven demand for series production cars is a bull-market phenomenon

Summary

Ferrari has operated at an extremely high level, and a good macroeconomic environment for asset prices has enabled the value of its existing cars to perform very well. From here, it is hard to imagine the brand’s market share in certain segments rising further; Ferrari’s ability to sell F80s highlights an opportunity for Porsche. As very large power outputs become commoditised, relative value will change. The most explosive asset price growth, as experienced by the F50, has come from (relatively) depressed valuations. To this extent, modern front-engine V12 berlinettas offer an attractive contrarian bet.